What Is Mortgage Prequalification, and Why Should You Care?

Let me break it down for you. Mortgage prequalification is like a sneak peek into your home loan options. It’s a quick, informal process where a lender evaluates your financial situation—your income, debts, and credit—to give you an idea of how much you might be able to borrow. Think of it as a trial run before you dive headfirst into the homebuying process. This step helps you understand your budget and sets realistic expectations so you’re not wasting time looking at homes that are out of reach.

Prequalification vs. Preapproval: What’s the Difference?

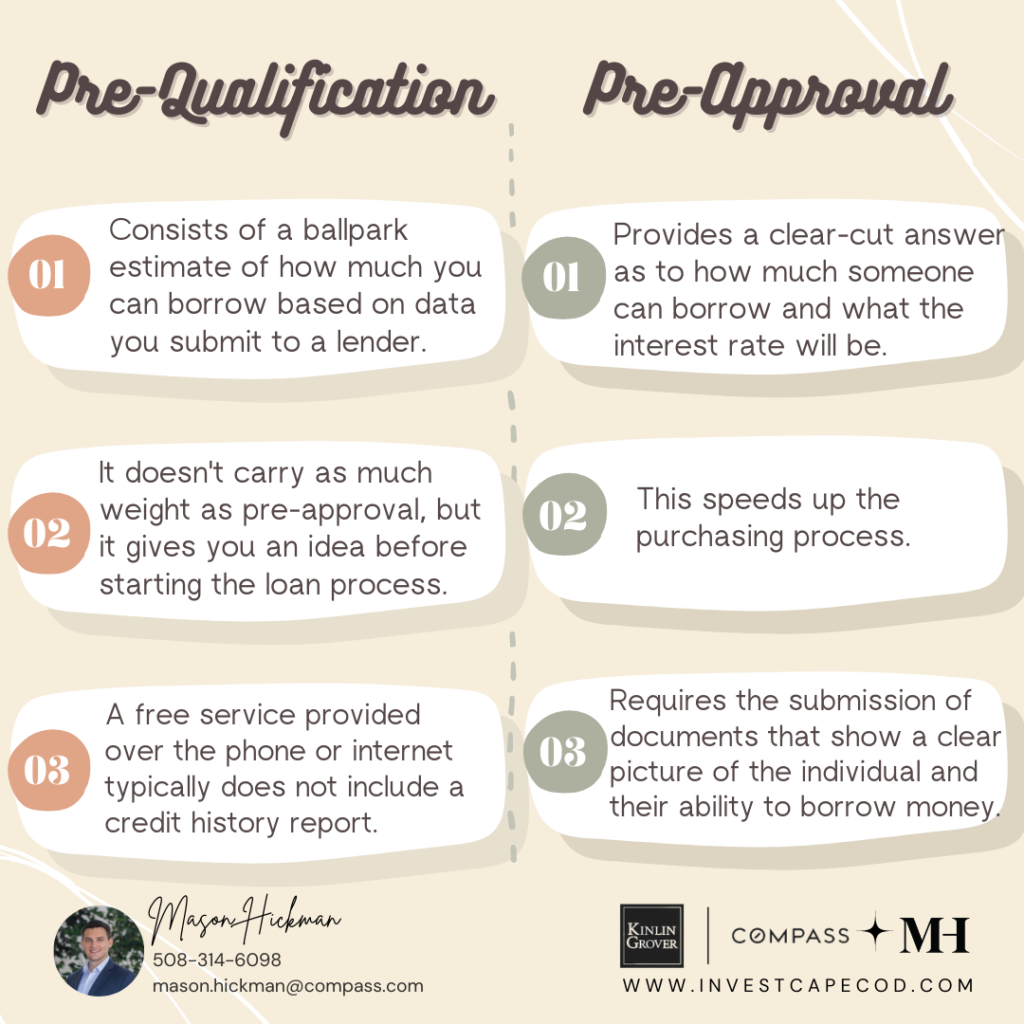

Now, let’s clear up a common confusion: prequalification and preapproval are not the same thing. Prequalification is more of a ballpark estimate—it’s a conversation starter between you and your lender. On the other hand, preapproval is a more formal process where the lender takes a closer look at your finances, verifies your documents, and gives you a conditional commitment to lend you a specific amount. If you’re serious about buying a home, preapproval carries more weight with sellers because it shows you’re financially prepared.

How to Get Prequalified for a Mortgage

Getting prequalified is pretty straightforward. You’ll need to provide some basic financial information, like your income, assets, and debts. Most lenders can give you a prequalification estimate over the phone or online in just a few minutes. It’s a no-obligation process, so there’s no harm in shopping around and getting prequalified with multiple lenders to compare your options. Remember, prequalification doesn’t involve a hard credit check, so it won’t affect your credit score.

Read also:Anahiacute And Televisaunivision The Inside Story On The Quieacuten Es La Maacutescara Scandal

Why Preapproval Matters in the Homebuying Process

Here’s the deal: if you’re serious about buying a home, getting preapproved for a mortgage is a must. It’s like having a golden ticket in your back pocket. Preapproval shows sellers that you’re a serious buyer who’s been vetted by a lender. It also gives you an edge in a competitive market because sellers know you’re ready to close the deal. Plus, it helps you avoid surprises later in the process by identifying any potential roadblocks upfront.

What Exactly Is a Mortgage Preapproval Letter?

A mortgage preapproval letter is your ticket to credibility in the homebuying world. It’s an official document from your lender that says, “Hey, we’ve reviewed your finances, and we’re confident we can lend you X amount of money.” This letter is your proof to sellers that you’re financially capable of buying their home. Just keep in mind that preapproval letters usually come with an expiration date, so don’t wait too long to start your home search.

Understanding the Mortgage Application Process

Alright, let’s talk about the mortgage application process. It doesn’t have to be as intimidating as it sounds. Here’s how it works: you’ll need to gather a bunch of documents—things like pay stubs, tax returns, bank statements, and proof of insurance. Once you’ve submitted everything, your lender will review your application, verify your information, and decide whether to approve your loan. The whole process can take anywhere from a few weeks to a couple of months, depending on the complexity of your situation.

Three Steps to Get Preapproved for a Home Loan

Ready to take the next step? Here’s a simple three-step guide to getting preapproved:

- Gather Your Documents: Collect all the necessary paperwork—pay stubs, tax returns, bank statements, and any other financial records your lender requests.

- Submit Your Application: Fill out the preapproval application with your lender. This can usually be done online or in person. Be honest and thorough when providing your information.

- Wait for the Decision: Your lender will review your application, verify your documents, and let you know if you’ve been preapproved. If there are any missing pieces, they’ll let you know what’s needed to move forward.

What Is a Mortgage Commitment Letter, and Why Does It Matter?

A mortgage commitment letter is like a promise from your lender that they’re ready to fund your loan, provided you meet certain conditions. This letter is a powerful tool because it shows sellers that you’re serious and financially qualified. It can also give you more negotiating power when making an offer on a home. But here’s the catch: the lender may require you to fulfill specific conditions, like providing proof of homeowners insurance or completing certain repairs before closing.

Preparing for the Mortgage Application: What to Expect

Before you dive into the mortgage application process, it’s important to know what to expect. Your lender will want to see a comprehensive picture of your financial health. This includes your credit score, employment history, debt-to-income ratio, and assets. They’ll also want to verify your information, so be prepared to provide documentation. The more organized you are upfront, the smoother the process will be.

Read also:Unlocking The Power Of Xnnn Your Ultimate Guide

Using a Mortgage Affordability Calculator

One of the first things you should do when thinking about buying a home is figure out how much you can afford. A mortgage affordability calculator can help you estimate your potential budget based on factors like your income, debts, and credit score. It’s a great starting point, but keep in mind that it’s just an estimate. For a more accurate assessment, consider speaking with a home lending advisor who can provide personalized guidance.

Understanding Mortgage Rates and Options

When it comes to mortgages, rates and options can vary widely. Some people opt for fixed-rate loans because they offer stability and predictability. Others prefer adjustable-rate mortgages (ARMs) because they can start with lower interest rates. It’s important to shop around and compare rates from multiple lenders to ensure you’re getting the best deal. Don’t forget to factor in additional costs like closing fees, property taxes, and insurance.

Tips for a Successful Mortgage Application

Here are a few tips to help you navigate the mortgage application process:

- Boost Your Credit Score: A higher credit score can lead to better mortgage rates, so it’s worth taking steps to improve it before applying.

- Reduce Your Debt: Lowering your debt-to-income ratio can make you a more attractive borrower and increase your chances of approval.

- Save for a Down Payment: While some loans allow for low or no down payments, putting more money down can reduce your monthly payments and interest costs.

Remember, every financial decision you make before getting a mortgage can impact the loan you’re ultimately offered. So, be mindful of your spending and avoid making major purchases or opening new lines of credit while your application is in process.

Refinancing: A Path to Lower Payments

If you’re already a homeowner, refinancing your mortgage could be a smart move. Refinancing allows you to replace your existing mortgage with a new one, potentially securing a lower interest rate or better terms. This can help you save money on your monthly payments and pay off your loan faster. However, refinancing isn’t always the best option for everyone, so it’s important to weigh the pros and cons before making a decision.

Final Thoughts

Buying a home is one of the biggest financial decisions you’ll ever make, but with the right preparation and guidance, it doesn’t have to be overwhelming. Whether you’re just starting your homebuying journey or you’re ready to take the next step, understanding the mortgage process can empower you to make informed decisions. So, take your time, do your research, and don’t hesitate to reach out to a trusted lender or advisor for help along the way.